By Francis Buttle[1], Julie Jones[2], Merlin Stone[3]

Customer relationship management (CRM) has been around for over thirty years, but there’s still widespread misunderstanding about what it is. That is partly due to competing perspectives – tech firms tend to equate CRM with the applications and tools that help marketing, sales and service managers do their jobs more effectively and efficiently. Functional managers in marketing might view CRM as campaign management. Adding to the confusion is the fact that CRM is largely absent from business school curricula which continue to teach established subject matter. Every business school offers instruction in marketing, for example. The supporting literature, research evidence, and course materials are well proven and widely available. Not so for CRM, regrettably.

In this series of four articles, we present a new model of CRM, the CRM Value Chain (CRM VC). The model aims to demystify, characterise, and conceptualise CRM, and eliminate the confusion.

What is the CRM Value Chain?

The CRM Value Chain (CRM VC) depicts our contemporary understanding of CRM as a set of strategic management practices that aim to drive profit performance. The focus of the CRM VC is on the profitability of customers, not the performance of brands or gross margins. CRM offers a customer-focussed way of doing business and is based on the notion that the primary purpose of a business is to create and keep profitable customers. If you can’t do that, then all you do is generate costs and losses.

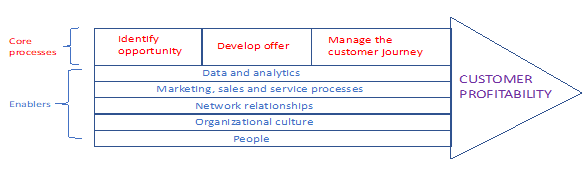

The Value Chain device has a history. It has been used to describe other value-generating, multi-step, processes. The device was first used by Harvard professor Michael Porter, and later by other Harvard professors, James Heskett, W. Earl Sasser, and Leonard Schlesinger. Our CRM VC differs from these previous models. It appears as figure 1 and shows that the primary purpose of CRM – indicated in the arrowhead – is to develop profitable relationships with customers. CRM is made up of just three Core Processes supported by five Enablers.

The three Core Processes are associated with value creation for both the business and customer. First, the business must identify an opportunity for value creation for specified customers, then, second, it must develop an appropriate offer that delivers the value that customers are seeking, and finally the firm must manage the customer’s journey towards and beyond purchase. The end goal of these Core Processes is to create and maintain profitable relationships with those specified customers.

The Enablers are the conditions or resources that support the effective functioning of the three Core Processes. One of the defining attributes of CRM is its dependence on data and analytics (Enabler 1). These allow marketing, selling and customer service processes (Enabler 2) to be more effective and efficient. Success in CRM is also dependent on the firm having successful relationships with members of its business network (Enabler 3). Organizational culture is another Enabler. Evidence suggests CRM produces stronger results in a supportive business culture. The fifth and final Enabler is people. Although a growing proportion of CRM initiatives are delivered by Artificial Intelligence, people are still critical in CRM. People develop and code the software applications that customer managers use; people interact with customers in storefronts, chatrooms and contact centres; people perform face-to-face sales and service roles.

Customer profitability

As shown in figure 1 the primary purpose of CRM is to initiate, develop and retain profitable relationships with customers. A profitable customer is one who generates more margin than it costs the firm to acquire, develop and retain that customer.

Business-to-business relationships

While it used to be the case that business-to-business (B2B) firms, particularly those with relatively few customers, had access to better data about customer-related costs than business-to-consumer (B2C) firms, the rise of online marketing, enabling direct selling to consumers, has allowed many B2C firms to understand the profitability of individual customers. This applies not only to consumer services such as utilities and financial services, but also to the online retailing of physical products.

Analysis of customer profitability data often shows that some customers are very costly to acquire and serve, others are not. Indeed, some customers may never become profitable. In B2B, for example, there can be considerable variance across several categories of cost:

- Customer acquisition costs. Some customers require considerable sales effort to shift them from prospect to first-time customer: more sales calls, visits to reference customer sites, free samples, engineering advice.

- Terms of trade. Price discounts, advertising and promotion support, extended invoice due dates.

- Customer service costs. Handling queries, claims and complaints, demands on salesperson and contact centre, small order sizes, high order frequency, just-in-time delivery, part-load shipments, breaking bulk for delivery to multiple sites.

- Working capital costs. Carrying inventory for the customer, cost of credit.

- Network development costs. Researching, recruiting, and managing customer-specific members of the business network.

B2B firms, particularly those who have implemented Activity-Based Costing (ABC), are often well-placed to identify gross margins and the associated marketing, selling and service costs with individual customers, giving clearer insight into the net margin or profitability of those customers. ABC splits costs into two groups: volume-based costs and order-related costs. Volume-related (product-related) costs are variable against the size of the order but fixed per unit for any order and any customer. Material and direct-labour costs are examples. Order-related (customer-related) costs vary according to the product and process requirements of each customer. Whereas conventional cost accounting practices report what was spent, ABC reports what the money was spent doing.

Business-to-consumer relationships

Marketing, selling, and servicing B2C customers usually takes place at market, segment, or cohort level. Margins and costs often cannot be allocated to individual customers. An exception would be the online pure-play retail firm that has a clear understanding of the net margins generated by each customer.

Even where B2C firms cannot trace costs to individual consumers, it may still be possible to allocate costs to segments or cohorts of customers. For example, a marketing campaign to acquire customers in new market segment might be able to allocate campaign costs to the acquired customers on a pro-rata basis. If the firm can identify the gross margins generated by these new customers, and the associated selling and service costs, it could compute the net margin or profitability of the segment. However, where it is impossible, too difficult, or too costly to identify net margin, the default position for CRM practitioners is to focus on processes and activities that deliver high gross margin.

Not all customers are or can be profitable

Not all customers are or can be profitable. This becomes clearer when businesses perform customer portfolio analysis (CPA). CPA assigns existing customers to different groups, so they can be offered different value propositions, or, in the case of there being no profit opportunity, no value proposition. The rise of digital marketing and mass customisation technologies now allow firms to customize offers to small segments or even individual customers. From a CRM perspective, it is critical to analyse and sort customers by profit potential, not by volume, whether that is by segment, cluster or individual.

Whereas much of the data used to compute or estimate customer profitability is historical, CRM’s aim to drive profit performance is also forward-looking. Businesses attuned to CRM are keen to identify and retain those customers who will deliver profitability in the future. This points to the importance of customer life-time value (CLV). CLV is the present-day value of all past, present, and future margins earned from a customer relationship.

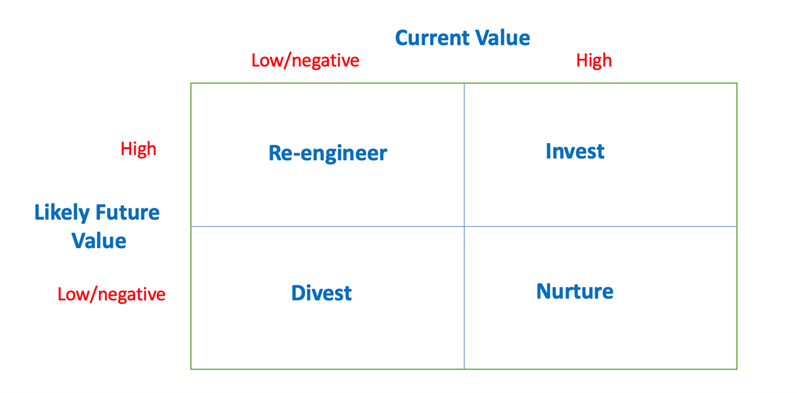

One CPA methodology clusters customers into 4 strategic groups – clear-out/divest, invest, re-engineer, and nurture – depending in their current and future value. Customers to be divested are those who have no present or future profit potential, in other words, no CLV. Customers who are too expensive to serve relative to gross margin, buy too little, make extraordinary demands on salespeople, require high levels of customisation, regularly switch to competition, pay late or habitually default may be “cleared out”. If they were employees they’ve be sacked. The ‘invest’ group contains customers who are both currently valuable and offer significant future potential. ‘Invest’ implies investment in ring-fencing the relationship. The ‘re-engineer’ group contains customers who are not presently profitable but who could become so if the relationship were re-engineered. Managing such customers better to achieve profit could focus on the causes of low value for the supplier and motivating or training the customer to fix the problems, perhaps leading to greater value for both sides. B2B options for the supplier may include cost-reduction strategies such as reducing the level of customer service, intermediation, or self-service through a portal instead of using a face-to-face sales team. The final, ‘nurture’, segment contains those customers who are currently profitable but have little future potential. One task here is to investigate, possibly in consultation with those customers, the reasons for profit pessimism. It may be that they can jointly find solutions which suggest a more profitable future relationship.

This CPA process enables firms to identify customers who are strategically significant. We can pinpoint five generic types of Strategically Significant Customer (SSC). First, the high future life-time value customer. This customer is financially very important and must be the focus of customer retention efforts. Many firms assume, often wrongly, that major customers who buy large volumes have high CLV. However, if they are costly to serve in the ways listed above, their CLV may be significantly reduced. One company that applied activity-based costing to allocate marketing, selling and service costs to customers found that two of their three biggest customers by revenue were in fact unprofitable. As a result, the company re-engineered its manufacturing and logistics processes for these customers, and salespeople negotiated price increases. Here, much can depend upon where the locus of control and relative expertise are in the relationship. Customers who are more expert than suppliers can be adept at taking control of the relationship and extracting value from suppliers, rather than the reverse.

The second type of SSC, high volume customers, whilst not necessarily being profitable, might still take on the status of SSC because they enable other customers to become profitable. They do this because of their absorption of a high proportion of fixed costs, and the economies of scale they generate to keep unit costs low. One oil-seed processor, for example, has two major customers, a manufacturer of snack foods which buys oil in bulk and a retail multiple which buys consumer packs. Although they account for 60% of oil-seed processing time, they absorb 85% of fixed costs between them, allowing the firm’s minor customers to become profitable.

A third group of SSC we identify are benchmarks. These are customers that other customers copy. A manufacturer of vending machine equipment is prepared to do business with a major soft drink brand at breakeven. Why? Because they can tell other customers that they are supplying the world’s biggest drinks vending operation. The fourth group are inspirations, customers who inspire change in the firm. These may be customers who find new applications, come up with new product ideas, or find ways of improving quality or reducing cost. They may be the most demanding of customers, or frequent complainers, and, though their own CLV is low, they offer other significant sources of value to the company.

The final group of SSC we call door openers. There are customers who allow a company to gain access to a new market. These customers are particularly important in certain circumstances, for example when a Western business wishes to enter an Asian market. The principle of Guan Xi, or relationships within personal networks, is very important in Chinese culture. It’s very difficult to do business in China without an established personal relationship.

Coming up

In our next article we will dig deeper into the three Core Processes in the CRM Value Chain, and in the final two articles we explore the five Enablers.

[1]francis@francisbuttle.com.au Formerly Professor of Marketing and CRM at Manchester Business School (UK) and Macquarie Graduate School of Management (Australia), Consultant in CRM, Customer Experience Management and Word-of-Mouth.

[2]jum1@aber.ac.uk Lecturer in Marketing at Aberystwyth Business School, Wales. Marketing Consultant and Chartered Marketer

[3]merlin.stone@stmarys.ac.uk Retired Professor of Marketing and Strategy, St Mary’s University, Twickenham, London, England

I’m very saddened to report that Professor Merlin Stone, who co-authored this and 3 subsequent articles with Julie Jones and me has died. He lost his battle with cancer on 17th July 2023. His daughter Talya tells the truth when she writes that “Merlin was a genius that brought intelligence and great energy to any room he was in. People loved to listen to him talk, and he took great pleasure in bringing together and helping people. He touched the lives of so many, and in his final days there could have been no greater love surrounding him.” Rest in peace, my friend, you lived well.