What a year it is!

2020 is surely a year worth remembering with a hard blow on the economy and businesses. However, COVID-19 has not been negative to all the businesses. There are some of the businesses that have managed to make a prominent mark, and the online payment system is one of among these.

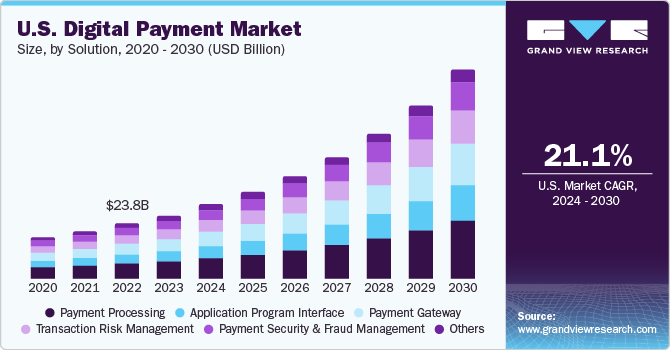

The fear of coming in contact with infected cash or check has encouraged individuals to look for a mobile money solution. According to a report, the global digital payment market is projected to register 17.6% through 2019-2025.

Well, this data was estimated before any hint of coronavirus. So, we can estimate that the vulnerability, in turn, strengthened the growth prospect of the online payments.

Top players such as PayPal and Facebook are eyeing to invest in digital payment market in Southeast Asia. This serves as a hint to how lucrative the digital payment solution is. As a result, search for cashless payment solution development would increase, and we would be witnessing new digital payment trends.

Top Trends that Would Influence the Online Payments in 2020 and Beyond

Below are some of the strong digital payment trends that would enhance the customer experience soon.

Biometric Authentication would be Mainstream:

The year 2018-2019 saw an incubation period for the biometric technology. However, it is 2020 when biometric authentication would be the most viable feature for the development of online payment mobile apps.

Following are the verification methods that would be prominent:

- Fingerprint scanners

- Facial recognition

- Iris recognition

- Heartbeat analysis

- Vein mapping

USP of Biometric verification: Customers today need a secure transaction, and biometric technology can offer accuracy, security and efficiency.

Switch from Card to Code:

The EMV technology—Europay, Mastercard, and Visa—has introduced customers to a more organized and computerized payment system. However, cards have their own set of limitations. You have to carry them with you. On the contrary, QR-oriented payments are quicker and are found to be resonating well with customers.

As a result, the present and the future of cards are gradually being overshadowed by cutting-edge QR based payment. Users can simply use their smartphones and process the payments.

USP of QR Codes: Cost-effective and instant payment mode for both—small shopkeepers and customers.

Online Wallet Solutions to Gain Traction:

Let’s go back by two to three years when wallets were a new thing in the peer-to-peer payment vicinity. Usually, all wallet payments would require users to transfer the money from their bank to wallets and wallets to peer.

Amidst this chaotic transfer of funds, the mediator would draw a commission on every transaction. As a result, users were kind of frustrated. However, today, peer-to-peer payment systems mean direct bank transfer. Wallets use other means to generate revenue.

In the quest to make cashless payment system user-centric, direct bank transferring wallets would accommodate a prominent position.

USP of Direct Bank Transfer Wallets: Users do not have to pay for any transaction.

Global Payment Support to Expand Internationally:

Most of the wallet-based online payment solutions have been operating at a local level. In such a case, it is essential to understand that today’s users need more of a global payment solution. While bank transfer assists the global transaction mode, the processing consumes at least 5-7 business days.

Customers of today need instant money. As a result, online payment solutions have to have global support, wherein users from different countries can transact money, and the currency conversion takes place automatically.

USP of Global Payment Support: Customers can transact money to users located in other countries for a low conversion fee.

Online Payments without Sharing Private Information:

The central authorities have red eye against companies that invade customers’ privacy by using their data. In the future, the norms of GDPR would turn stringent to a grade or two. In such a situation, some companies are looking for a digital payment solution that can process a transaction without using personal data of customers.

By personal data, customers wouldn’t even want to share their email ids and phone numbers. As a result, the futuristic mobile payment solutions would mean the encryption of customer information.

USP of Encrypted Payment Accounts: Users would be able to transact without having to share their email ids and phone numbers.

The BIGGEST Digital Payment Trend is to be Simple

Now that we have seen five of the most influential digital payment trends that are going to affect businesses in 2020 and beyond, what do you think is the common thread pulling all of these together?

It is customer-centricity and simplicity.

More complicated an online payment solution, higher is the probability that you would lose your customers. Take, for example, the wallets that charged money to transfer fund to a bank account. It is complex and time-consuming. In a way, paying in cash is simple than this.

As a result, when online payment solutions with direct bank transfer were developed, they pickup up the pace, and today they are booming.

So, next time, you want to build a peer-to-peer payment mobile application, think of a simple process to survive and succeed in the business.