Consumer behavior saw major shifts in 2020 and 2021, and it’s no secret that this year has brought on more changes. While the COVID-19 pandemic fueled much of the initial upheaval, more recently, labor and supply shortages, geopolitical tensions, stock market volatility and inflation have grown to be dominant forces. Inflation has been the leading driver of differences in consumer behavior.

Inflation’s role in consumer purchase decisions

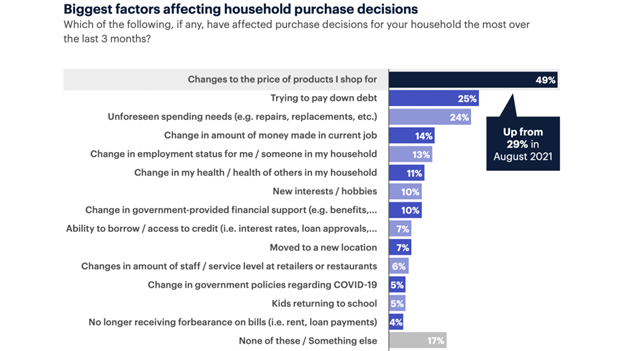

Based on Medallia Market Research, of the many factors capable of influencing household purchase decisions, 2022 saw “changes to the price of products” ranking in a clear top spot out of over a dozen choices, including things like paying down debt and unforeseen spending needs. In addition to outranking the other factors substantially, “changes to the price of products” also grew over 20 percentage points compared to summer 2021. For those who once presumed factors like COVID-19 safety concern, remote work-driven migration, or reduced staffing at retailers are playing just as big a role as price itself, the data suggests otherwise.

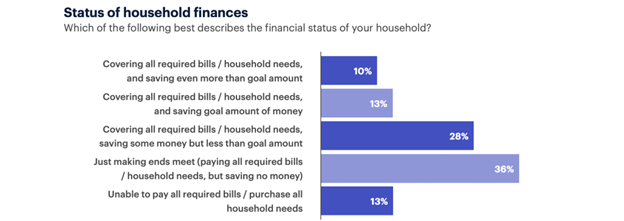

It’s no surprise when recognizing the little ability consumers have to keep up with prices, as less than 10% say their salary or wages increased more than the rate of inflation over the last year (that is, by more than 8-9%), and, at the same time, only 23% of consumers say they’re able to cover all of their bills and meet or exceed their goal savings amount, a clear indicator that price changes are very much correlated.

Is inflation changing purchase behavior?

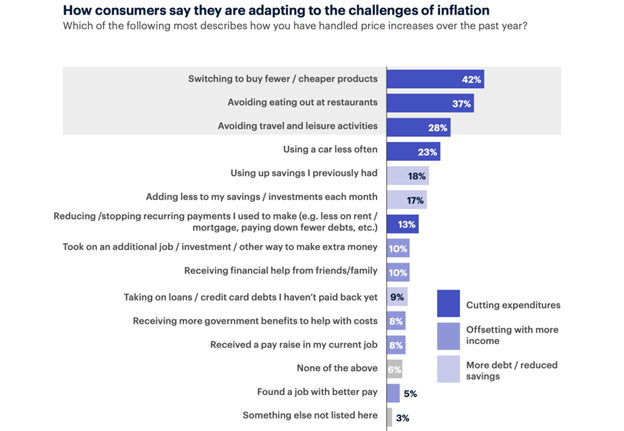

With only a small minority of households finding ways to increase their incomes to adjust to the effects of inflation, the remainder have generally cited a turn to reducing expenses among the other available options. Trading down to cheaper products or buying fewer of them was cited as the most common approach, with cutting back on restaurants and on travel and leisure.

Additionally, a portion of the population is turning to less sustainable approaches like using up savings or taking on loans they have not yet begun to pay off – collectively this group who indicated at least one of their top three actions includes reducing savings or adding debt makes up 37% of the total population.

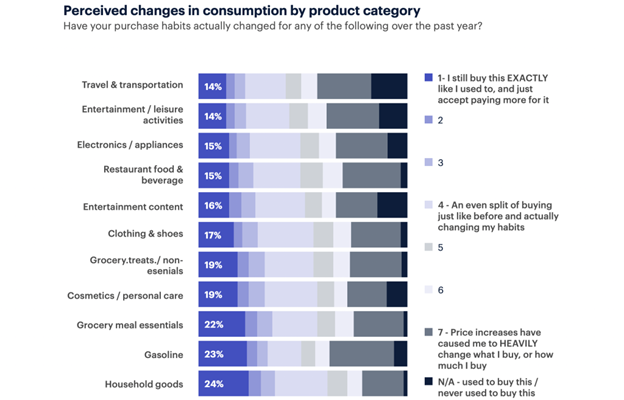

With regards to cutting back on expenses across some product categories more than others, it appears consumers are taking that approach. Data found that there is a general behavior of cutbacks on the “nice to haves” in favor of the “need to haves.” Gasoline is especially insensitive to consumption changes, despite having one the largest increases in price compared to 2021. Daily commuting also seems impossible to modify for many consumers, leaving other expenses like leisure and hospitality and some forms of food and beverage consumption on the chopping block more often.

In analyzing the spend behavior of over five million credit and debit card panelists and comparing today’s data to 2019 baseline levels, the cutback on everyday purchases is validated. Consumer transactions at restaurants and grocery stores slowed down in the first half of 2022 after being up by the end of 2021 compared with spring 2020 levels. Because prices have increased, however, overall spend per transaction is up. Despite restaurant food being perceived as more of a treat than groceries, the transaction volume cutbacks for restaurants and grocery stores have been near equal. This is likely because price increases for groceries have, in many cases, been even more severe than restaurant price increases.

What might a further increase in the inflation rate due to consumer spending?

Consumers indicate they can’t tolerate more price increases from here – nearly all say another five percentage point increase in the inflation rate beyond current levels would be met with drastic changes to their shopping decisions. Considering the cited inability of many households to make ends meet currently, this is not a surprise.

However, there may be light at the end of the tunnel for business owners stressing about their consumers’ ability to pay in the future. The acceleration of the inflation rate has been less severe in recent months (that is, month over month growth is less severe than it was in late 2021 and early 2022). Recently, daily polls of Medallia Market Research panelists shows that factors like the “price of products” has not further increased as a driver of household purchase decisions, though it still ranks number one.

If the inflation rate holds at levels like recent months, 2023 could not only be met with a continued trend of consumers moderately cutting back on purchase frequency of several product categories, but purchase frequency also could slightly worsen if the cohort of customers tapping into debt or savings finds this behavior unsustainable. Changes to interest rates and average wages may end up being especially important factors.

With the exact changes in the inflation rate over the coming months lacking certainty, one of the best things a brand can do is understand both shopper decision-making and how sales performance is trending compared to competitors. Even if inflation causes transaction declines due to consumer cutbacks, a brand may still be better off riding its current course compared to taking drastic action that could hurt profitability even further. Without seeing the data of what strategies appear to be working well for competitors and which to avoid, a brand is left flying blind.