Source: Pixabay

An Insurance policy should give us confidence that we and our possessions are taken care of, at a time of need. If something does go wrong, and customers make a claim, our chosen insurance company be helping to get life back on track at difficult times – not making life harder.

Our daughter, who passed her driving test 8 months ago, turned 18 in early February. Unfortunately, she was recently involved in a no-fault collision on her way to school. This first accident was stressful for all concerned. As if her life wasn’t busy and complicated enough, as she is nearing her A-levels and moving away from home to go to Medical School in September.

According to research by Accenture, a staggering 83% of customers who had made an insurance claim and who had reported a dissatisfaction with the way their claim was handled, said they had switched or planned to switch to another insurer. A claim is clearly a key moment of truth/ a make or break time for customers. Claims are also an opportunity for insurers to deliver great customer service and an elevated customer experience.

I can associate with Accenture’s survey respondents, right now. I had hoped that the insurance policy that we have taken out for our daughter would respond and simplify an all too common event, as the insurer’s processes kicked into place. Car accidents are unexpected, high-stress experiences that can leave insurance customers in a state of confusion and anxiety. Dealing with your car insurance claim should be straightforward, easy and efficient, but unfortunately, as we have found, it is often a major inconvenience.

Handing the customer off to someone unreliable

Despite buying the policy from one insurance brand, we were immediately passed over to their outsourced claims partner. This third party claim’s administrator is used to help ‘improve operational efficiencies (for insurance companies) and to consistently demonstrate service excellence (to customers)’. This ‘passing over’ was unexpected. I, possibly naively, thought that by buying a policy from the insurance company that they had a responsibility to deliver the very product (claim service) that I had paid in advance for. It appears, however, that they have no interest when things go wrong.

The subject for this piece isn’t the time consuming and arduous experience of proactively coordinating the moving parts of this claim ourselves and engaging with their designated partners to move the claim forward. The feature of my writing has arisen from a process failure of the outsourced partner, that led to disruption and angst.

Exhibiting a complete lack of empathy

It took 5 days to get a replacement car. There were a number of reasons to do with our daughter’s age, the cover and her authorisation, but we eventually got one.

We duly completed and returned the required hire agreement for this courtesy car so that she could be up and running as soon as possible. That’s when some of the problems began. We had a call from yet another unknown company, telling us that because we had failed to return said paperwork, that they were coming to collect the paperwork directly from us. We explained that we had sent off the documents and scanned copies and offered to repeat the process for them – as clearly their moving parts in the process had lost them.

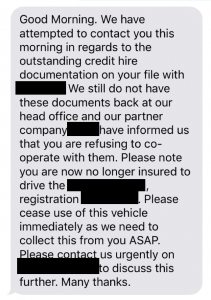

Yesterday morning, I received a troubled message from my daughter at break time. She had received a text, despite us asking all parties to liaise directly with us (her parents). The text is to the left:

Yesterday morning, I received a troubled message from my daughter at break time. She had received a text, despite us asking all parties to liaise directly with us (her parents). The text is to the left:

Can you imagine the shock, fear and distress that this has caused? She is at school with no credit card and now stranded with no means to travel the 25 miles home after school. Shame on you, insurance company.

The tone of the message is perturbing. “Please cease”, “no longer insured”. For “refusing to co-operate”, or, if you can’t manage to get through on one of our many different numbers to any one of our many anonymous people who are all on the phone, when you are not in lessons and during our working hours.

This is totally unnecessary. Their left hand does not know what their right hand is doing. This organisation has been disorganised, unhelpful, unresponsive and rude – and now has shown a complete lack of empathy and consideration.

Putting customer out (again)

I was about to publish but I felt compelled to add today’s episode of this troublesome Customer Experience saga.

We once again scanned and sent off the documents to now a named person who seemed to be taking ownership of the issue. They agreed not to bother our daughter again and that things were now resolved.

Imagine, our annoyance this morning when our daughter received a text message from the 3rd party of the 3rd party of our insurer (keeping up? we have struggled) to collect said documents that we though they no longer needed. The guy confirmed to our daughter on the day, whilst at school that he would be at our home (25 miles away) at 2pm today. Fortunately, I was working locally and came back from a meeting specially, arriving on time. The collector, despite confirming 2pm, arrived early and then showed his annoyance directly to our daughter because I wasn’t there and that he couldn’t wait any longer for personal reasons. For the Brits, amongst you, piss up and brewery come to mind. We are now arranging to have the documents couriered to them so they will have at least 4 versions of the same thing in differing areas of their business. What an epic failure.

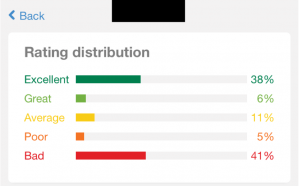

Averaged scores hide poor experiences

I looked up our insurer’s partner’s rating on TrustPilot. They don’t look too bad at first sight. They score 3 stars out of 5. But when you dig deeper, the real picture is exposed. Their overall score is 5.6/10 which is not good and doesn’t give you confidence in such an important risk product. They are 196/203 in their category. Yet, my actual insurer clearly thought that they were up to the job – maybe that’s why they don’t tell you up front that that parts of the customer journey such as claims, vehicle hire, body work, settlement values are being outsourced.

What’s more, the distribution of their ratings reveal an inconsistent customer experience.

So, it you looked at this as you would nps, Excellent and Great add up to 44% and Poor and Bad to 46% – net a score of -2.

On reading their reviews, some people have had a good experience. Others have had bad ones, like ourselves. So the scores have resulted in an ‘averaging out’ and hides the true picture. Like many experiences, customers are being subjected to a lack of consistency in this organisation’s delivery – yet our insurer is choosing to partner with them.

Experiences must get better for customers

I recognise that even the most deliberate, seamless claims process can be derailed by something that begins as a relatively minor problem and is then exacerbated by the accumulated stresses of the initial incident and the claims process.

At the very least, insurers need to improve the basics if they are to hold on to their customers and ensure a better experience. These 10 things would have helped our experience and made it a vastly better one:

For Happy Customers:

1. Manage and set customers’ expectations to ease their anxiety

2. Be transparent about the claims process – what will happen, who will be involved and how long it will take

3. Make the whole process simple, speedy and above all effortless on the part of the customer

4. Openly and visibly show your support for your customer even if you have handed them over to a partner organisation

5. Make it clear who is owning their problem and how they can easily access help

For Smiling Companies:

1. Map the lived customer journey based on real evidence including all your chosen partners and stakeholders

2. Work back to the internal delivery processes, systems, people and behaviours that are causing problems

3. Prioritise pain point fixes that will have greatest impact for the customer

4. Be more customer friendly in interactions and communication and less process oriented

5. Make sure that someone takes ownership of the customer and their problem through to resolution and closure

We are left feeling frustrated and frankly exhausted. We have been left alone by our insurer and handed over to inconsistent and unreliable partners. The experience and our journey so far has been a shambles. Our insurer has not once followed up since the initial accident reporting to show interest and demonstrate that they care. This could not have been much more complicated or stressful that it has been. We worryingly still have some way to go before the claims process is complete.

As it stands, I will be one of the 83% of customers who will look elsewhere when this experience is over and I doubt our insurer will notice, or even wonder why.

Hi Amanda,

wow, what a nightmare! Sometimes, it’s really a miracle how companies like that do remain on the market. Your experience seems even worse than the one I had recently, trying to buy a fridge:

https://iwantmyname.com/blog/what-a-fridge-has-taught-me-about-customer-support

I keep my fingers crossed for you, hopefully, that insurance company will get their things sorted. Finally!