Project management ideas can sound complicated at first. You’ll read lots of jargon about inputs and outputs, your WBS, measuring PVs against your EVs, KPIs and OKRs according to the PMBoK… but a lot of it is just systemizing common sense.

Whether you want to run a marketing campaign, onboard a new hire, or even submit your VAT return online, having very clear processes to follow ensures consistent performance across the business and helps the team get things right every time.

Project cost management can look like a minefield. But once we’ve broken it down step by step, it’s much easier to get your head around.

What is project cost management?

Project cost management is how project managers, teams, and businesses stay on time and under budget. They avoid running over budget, de-risk complex projects, and track and improve the way they work over time.

It’s about staying on budget. But done right, it’s also about keeping big teams on the same page and becoming a better business in the long-term.

Why is it important?

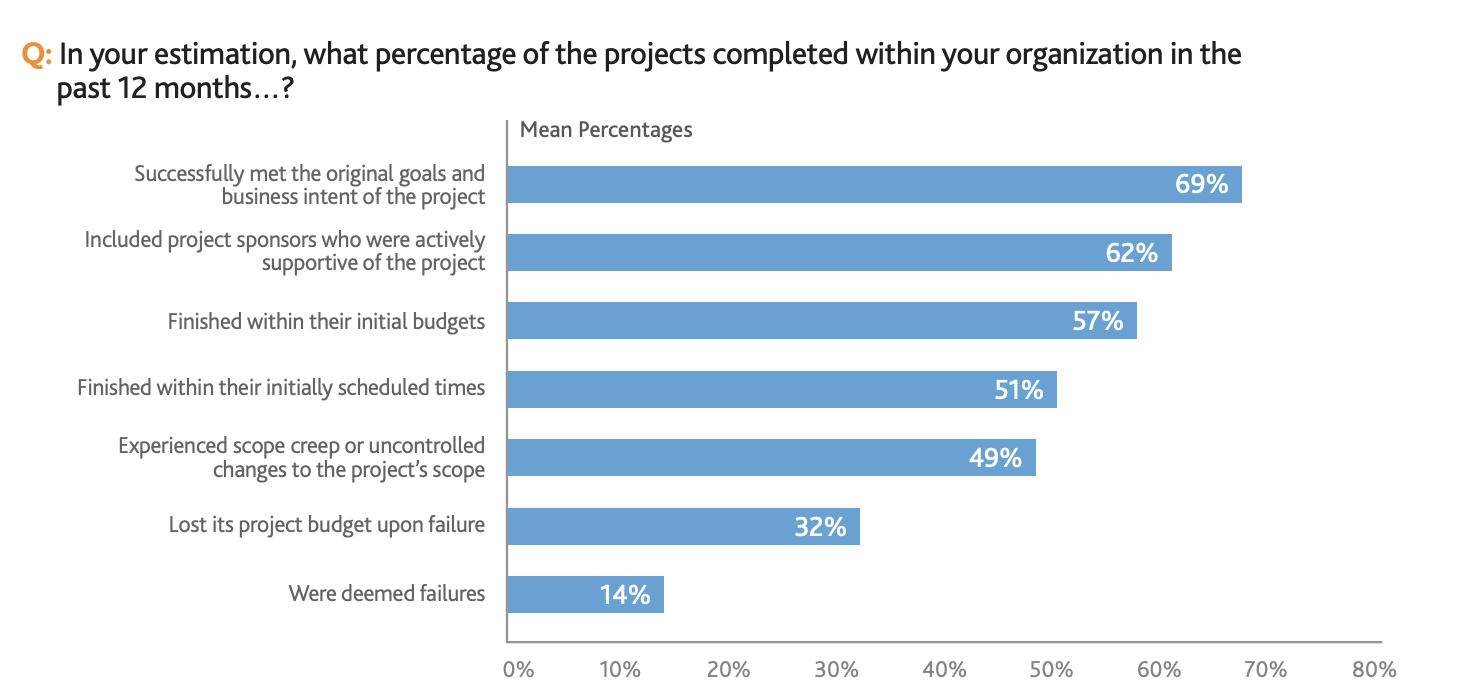

It’s easy to assume that everyone else is on the ball with this. But without following a strong project cost management process, it’s easy to run into problems.

PMI found that only 57% of IT projects stayed within budget. In the world of construction, where costs are high and controlling budgets is so important, McKinsey found that companies delivered projects 30% over budget and one year late on average.

Project cost management helps you build a more efficient and reliable business and make better decisions. It also helps you learn from mistakes that inevitably happen.

Teams can work with confidence that things are going according to plan, and know how much room they have to adapt if something doesn’t. Clients can rest assured that their money is being spent well, and you can check on complex projects at a glance.

Sounds good? Let’s look at it step by step and see some best practices.

Best Practices

In the Project Management Body of Knowledge—or PMBoK, pronounced “pimm-bok”— project cost management consists of four processes. For our purposes, we can condense that down to three sequential stages: Planning, implementation, and analysis.

Planning

At the planning stage, you’re just tallying up the projected costs on different steps of the plan. You’ll also consult with stakeholders to make sure everyone is clear on what will be spent and where.

You’ll be answering questions like: How much room for variance is there in our budget? What’s the planned value (PV) of the things we’re trying to build, and how do we measure that value?

You’ll be taking stock of the resources you have and deciding what new resources might be worth investing in. You’ll also want to look at cases where project costs have overrun in the past, and what you might learn from them. We’ll get back to that later.

We’ve mentioned project cost management in IT and construction, but any team can benefit. Marketers, for example, will have to consider SEO pricing which involves different pricing models, which activities would be most valuable to your business, and how you’ve successfully spent the marketing budget before.

Implementation

Once you get started, you’re in the implementation phase, where you’re actually spending money.

Where others might just hope things go according to plan before they have to answer for it all at the end, proper project cost management—with clearly-defined phases, budgets, timelines, margin for error, etc.—allows your team to adapt on the move.

Such a detailed breakdown allows you to closely monitor what’s being spent and when, against what was planned, and measure how much value you’re really getting out of that spending, compared to what you estimated.

Best-case scenario, this means you can see parts of the project which your team has underspent on and move that money around to where it’s better spent.

If things go wrong, you’re still better off for having these processes in place. A clear fault tolerance (say, you’re allowed to go 10% over budget on certain materials if you have to) enables managers to make quick spending decisions autonomously.

This saves them having to stop work to consult you, then you having to stop to consult your manager, and your manager having to stop to ask their manager, every time something comes up.

In a complex project, it’s easy for one person to make a rash decision that starts a domino effect knocking the whole project off-track. Project cost management gives everyone the confidence to react to changing circumstances in an agile but careful way, ensuring that nothing is left underfunded and that good records are kept on any changes.

That data will be important when you get to the analysis phase.

Analysis

Dwight D. Eisenhower said in 1957 that “plans are worthless, but planning is everything”. This is often mixed up with an 1871 letter from Helmuth von Moltke, which read: “no plan of operations extends with any certainty beyond the first encounter with the main enemy forces.”

So what’s the use of project cost management if we accept that things are going to go wrong?

Where most people think they’re finished, project managers enter the analysis phase. This is where you look back over the project and compare your plan to the detailed records it lets you keep of what happened, when, and why.

You’ll compare the planned value (PV) of different steps and investments to the actual earned value (EV). You’ll also see what tasks fell behind schedule and why. You can then discuss with your team what you’ve learned and how to improve cost management on your next project.

That could mean looking for new contractors to work with, or software to use. It could mean improving the way different teams communicate or streamlining processes.

Automating routine tasks like invoicing or adding an employee to payroll seem like small improvements, but those add up to more streamlined, predictable projects with less chance of human error causing setbacks.

What’s next?

As the PMI and McKinsey studies show, project cost management is much easier in theory than in practice. It’s important to develop consistent, repeatable processes and to learn from mistakes you’ll make early on.

The whole point of the exercise is to enable you to analyze project spending in detail and keep improving your business’ processes over time.

Project cost management, like anything else in project management, can sound quite abstract at points. But as you get more familiar with these practices you’ll see them translate into healthier profits, less stressful projects, and happier employees who have learned to get complex work right every time.