Marketo made good today on its promise to file for an initial public offering (IPO). Congratulations to them for reaching this step. It’s a major accomplishment.

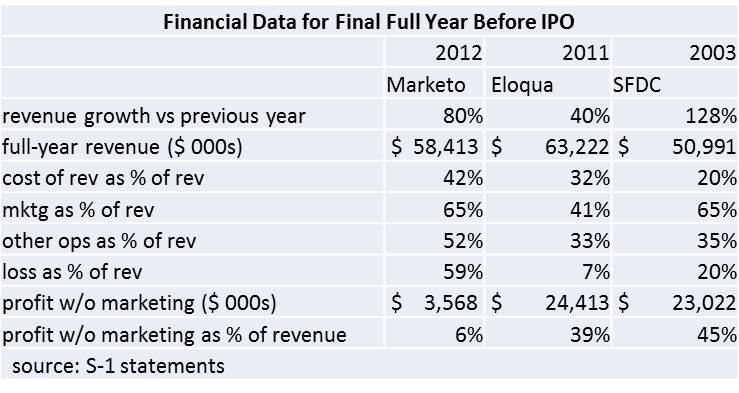

The S-1 registration statement gives considerable new information about Marketo’s business. Revenue for 2012 is reported at $58.4 million, an impressive 80% growth rate vs. 2011 although not quite the doubling that the company had forecast earlier.

More significant, the company continues to have huge losses – it lost $34.4 million in 2012, or 59% of revenue. By comparison, Eloqua lost just 7% of revenue in the year before its IPO, and even Salesforce.com, the benchmark for all Software as a Service (Saas) start-ups, lost just 20% of revenue in its final year as a private company.

A loss that big is pretty scary. Part is due to heavy spending on sales and marketing – 65% of revenue – but that’s not the whole story: Salesforce.com had also spent 65% on marketing before its IPO (although Eloqua spent just 40%).

The difference is that cost of revenue (costs of delivering service to clients, including subscription, support, professional services, and other) was 42% for Marketo, vs. 20% for Salesforce.com and 32% for Eloqua. That figure hasn’t changed in recent years, suggesting economies of scale have yet to appear. A high cost of revenue makes it hard for a company to become profitable even as it grows, since much of the new revenue is spent on the new customers. SaaS economics aren’t supposed to work that way.

Marketo’s other operating costs (research & development and general & administrative) are also high – 52% of revenue, compared with 35% for Salesforce.com and 33% for Eloqua. That percentage has also been pretty much stable for the past three years – again suggesting that expected scale economies haven’t appeared yet.

Another way to look at it is this: Marketo would earn just 6% profit even if its sales and marketing costs were zero. So its losses aren’t simply due to high investment in new customers.

The S-1 also reports the company had 339 employees as of December 2012. Of course, the average for the year was much lower but, ignoring that, this still yields a perfectly respectable $172,000 revenue per employee. But it also means expenses are $273,000 per employee – much higher than the $200,000 rule of thumb. I know everyone at Marketo works incredibly hard, but something is clearly out of line in their cost structure.

Perhaps stock investors will look only at Marketo’s growth rate. There is certainly an argument that the company will eventually become more profitable as it spreads its fixed costs over more clients. Let’s the stock market sees it that way: Marketo stock will be much harder to sell than its software.

{kind=link}