Rising inflation, an uptick in interest rates, and soaring cost-of-living are prompting savvy-savers in the U.S. to make decisions regarding their deposits such as dipping into hard-earned savings and cash reserves, or switching to more competitive accounts.

New FICO research reveals how consumers’ saving behaviors have changed amid volatile times, including their change in expectations and their tendencies to shop around to get the most competitive deals for their hard-earned deposits – even if it means switching to a relatively unknown neobank, fintech, or an online only bank. In fact, up to 67 percent of consumers readily admit they’re interested in switching to accounts that offer more personalized deals and advice to help meet shared savings goals.

Consumers are now looking beyond their legacy banks to cash in on competitive promotional savings offers elsewhere. FICO research indicates that 30 percent of consumers opened new accounts outside of their primary bank within the past year and 46 percent of consumers now use such accounts instead of accounts with legacy banks.

Convenience Plus Competitive Products and Offers Are Keys to Unlocking Savings Deposits

FICO research reveals more than one in four consumers already favor the convenience of online banking. At the same time, there is a clear migration towards lean, agile, and new-to-market FinTechs and digital providers that are unburdened by the overheads of maintaining legacy back-office systems and costly branch networks.

Despite ‘traditional’ banks retaining many consumers’ primary accounts, many enterprises are missing out on a sizeable market share of savers’ deposits (given the breadth and scale of incentives available elsewhere). It’s a trend being further compounded and hastened by the move to shelve customer overdrafts and spending buffers.

Improving Financial Wellness by Innovating Savings and Deposits with Support and Incentives

As the squeeze on incomes continues, banks that offer new or alternative routes to meet their customers’ needs – by directly helping them on their financial journey or by easing cash-flow burdens – will be well regarded by many consumers. It also underpins banks’ customer retention initiatives. Despite only 37 percent of consumers indicating they are currently saving with a specific target in mind, around half of those want to be able to keep track of their progress directly through their bank. By offering support that incentivizes savings with rewards and encouragement en route to consumers’ goals, banks can outshine the competition.

Three Quick Wins to Retaining Savvy-Savers and Safeguarding Market Share

Right now, traditional banks have a golden opportunity to boost their market position and retain their best-performing customers. However, success hinges on flexibility, competitive offerings, and collaborative partnerships that help customers reach their financial goals and savings aspirations. It’s not simply a matter of delivering a market-leading interest rate, but also delivering additional solutions that help ease the financial strain on any under-pressure customers.

If banks fail to transform to meet consumer expectations, hard-won customers will simply go to a financial services provider that can. The following three steps should be evaluated and considered to retain customers and market share:

1. Plug in to data and analytics to help point the way.

Many savvy-savers made the most of the pandemic by hoarding unspent cash in savings and deposits. However, now as the economy has opened, banks are obliged to re-think how they hang on to their best customers. FICO helps by enabling financial services providers to plug in to data and analytics to quickly determine the best offers, deals, and acquisition strategies that will help win, retain, and safeguard market share.

2. Complacency costs in lost business.

Don’t fall asleep at the wheel! While many customers may be willing to continue using primary and checking account offerings, many will be tempted by competitive offers elsewhere. Be prepared to leverage all available customer data to offer personalized offers that continually meet the needs of consumers, regardless of where they are on their financial journey.

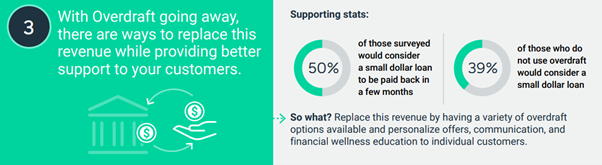

3. No more overdrafts? No problem! Innovate with alternatives.

Despite the long-overdue overhaul of overdrafts, there are still quick wins for banks to support their customers. This may include contingency planners covered by pre-agreed lines of credit, or links to deposit accounts. Alternatively, the flexibility of grace periods, a modest cash cushion, or self-selected customer repayment options could be considered. Sudden and unexpected expenses could also be covered by so-called small-dollar loans, exception authorization, or an extended cash cushion in some circumstances.

Learn more about how to improve market share and customer retention here.