For the past few weeks, the hottest topic in the business/financial media has been whether the U.S. economy is headed into a recession. Every day, a parade of economists, market analysts and other pundits appear online, on TV and in print to give their view on the likelihood that a recession is on the horizon.

In addition, several major Wall Street investment firms have recently estimated that the odds of a recession occurring in the next several months have increased.

The odds of recession are increasing primarily because the U.S. Federal Reserve is tightening monetary policy in an effort to rein in historically high levels of inflation. Since the beginning of this year, the Federal Reserve Open Market Committee has raised the target federal funds interest rate 2.25%, and it has recently started reducing the size of the Federal Reserve's balance sheet (which tightens financial conditions).

The Committee has also indicated that additional interest rate increases are likely, and most Fed watchers are expecting an increase of 0.5% at the Fed's September meeting.

Marketers need to have a reasonably accurate picture of future economic conditions in order to develop sound marketing plans. As I've previously written, the health of the overall economy is one of the major factors that create the environment in which marketing plans will be executed. And while macro economic conditions affect different kinds of companies in different ways, they will impact the success of marketing efforts at most companies to some extent.

Unfortunately, the outlook for the U.S. economy over the next several months is far from clear. The uncertainty exists for several reasons, including the real-world impact of Federal Reserve's policy decisions, the continuing problems in global supply chains, and a possible energy crisis in parts of Europe this winter.

Given this high level of uncertainty, the best option for marketers is to focus on those future economic conditions that can be predicted with a reasonable degree of confidence. In my view, we can say two things about the direction of the U.S. economy over the next 6 to 12 months.

- Economic growth (as measured by real GDP) is likely to be slow even if we are able to avoid a recession.

- Inflation is likely to be persistent and remain above the Federal Reserve's target of about 2% per year, although there are some indications that we may already be past the peak of inflation.

Economic Growth

Real GDP growth slowed significantly in the first half of 2022. The following chart shows the trailing 12 month rate of real GDP growth measured at the end of the four most recent calendar quarters.

At the end of Q4 2021, the real GDP growth rate over the preceding 12 months was 5.5%. By the end of the second quarter of this year, the annual growth rate had fallen to 1.6%.

Most economists are predicting slow economic growth in 2022 and 2023. For example, the latest (July) forecast by The Conference Board is that real GDP will grow 1.7% in 2022 and 0.5% in 2023. (Note: Many economists say the long-term sustainable growth rate of the U.S. economy is about 2% per year.)

Below-average growth over the next several months is the most likely scenario because it is difficult to envision any events that would trigger an increase in economic growth in the short run.

Inflation

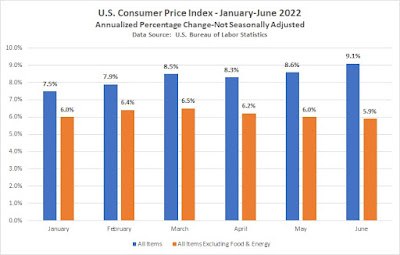

Inflation has emerged as the most serious issue currently affecting the U.S. economy. The following chart shows the annualized rate of inflation for January through June of this year as reported monthly by the U.S. Bureau of Labor Statistics. The chart includes both the "headline" rate of inflation (All Items) and the "core" inflation rate (All Items Excluding Food & Energy).

The substantial and persistent gap between headline and core inflation shown in this chart demonstrates that high fuel and food prices have been major contributors to inflation this year. This, of course, won't be surprising to anyone who drives or eats.

On a positive note, there are some indications that inflation may already be easing. For example, as the above chart shows, the core inflation rate has been declining since March. In addition, AAA has reported that the national average price of gasoline fell from $4.85/gal on June 30th to $4.21/gal on August 1st. These declining gasoline prices should be reflected in the July consumer price index, which the Bureau of Labor Statistics will release on August 10th.

Even if inflation has already peaked, many economists and other analysts are forecasting that the rate of inflation will decline only slowly. In June, Federal Reserve Board members and Federal Reserve Bank presidents predicted that PCE inflation* in 2022 would be 5.2%, still substantially above the Federal Reserve's target inflation rate of 2%.

Key Takeaways

For marketers, the key takeaway here is that economic growth is likely to be sluggish for the next several months. The outlook for inflation is generally favorable, but energy market analysts have noted that most physical energy markets are still tight. Therefore, there is a substantial risk that energy prices could rise later this year and slow the progress on inflation.

*PCE inflation is the percentage rate of change in the price index for personal consumption expenditures. PCE inflation is generally considered to be the Federal Reserve's "preferred" measure of inflation.

Top image courtesy of CreditDebitPro.com via Flickr (CC).