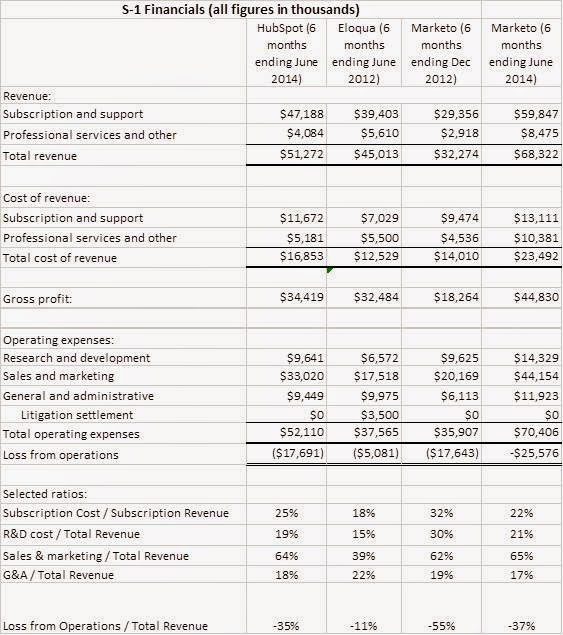

- loss equal to 35% of revenue, compared with 11% for Eloqua (which was run very conservatively) and 55% for Marketo (which was highly aggressive).

- high absolute revenue level (well on track to exceed $100 million for the year, about 20% higher than Eloqua and 60% higher than Marketo at the time of S-1).

- subscription and support costs are 25% of subscription revenue, in between Eloqua and Marketo. (This ratio is important because it hints at the profitability of on-going operations regardless of sales costs. Marketo has made great strides in bringing it down since their S-1. Marketo’s R&D costs are also now more in line, at 21% of revenue. In fact, Marketo today looks a lot like the HubSpot S-1.)

- sales and marketing costs at 64% of revenue, well above Eloqua (which was growing much more slowly) and similar to Marketo (which was growing slightly faster).

The basic picture, then, is a disciplined company that has grown quickly while keeping costs in line. As I say, pretty much what we suspected.

The S-1 does provide some other insights – in particular, highlighting HubSpot’s shift in focus from very small businesses to mid-size business. The following table, taken directly from the S-1, shows this clearly: revenue per customer has climbed steadily from $5,395 in 2011 to $8,823 in the first half of 2014 – a 64% increase. Still, the average revenue per client is well below Marketo, which is in the $30,000 to $40,000 range.

The S-1 also reveals that agencies and agency referrals accounted for 42% of customers and 33% of revenue for the six months ended June 30, 2014 – meaning that agency clients tend to be smaller than average. I’d expect HubSpot to have more direct sales as it engages larger clients, but that doesn’t seem to be the case, at least yet: compensation to agency partners grew by $1.2 million for all of 2013 and by $0.9 million for the first half of 2014, suggesting a 50% or better increase for the year as a whole. This is roughly in line with over-all revenue growth.

In fact, the only thing that struck me as a bit odd in the prospectus was HubSpot’s frequent description of itself as an “all in one” marketing and sales solution – a term more usually applied to micro-business specialists like Infusionsoft and Ontraport, which combine marketing automation with CRM. HubSpot does make several references to supporting sales departments in its document, which a casual reader might interpret to mean it also provides CRM features. But this is something the company has adamantly refused to do for years, despite pressure from its original small business clients and the partners who serve them. It makes even less sense when selling to the mid-market. The prospectus does eventually state that its sales features are designed to integrate with CRM, but the ambiguity is atypically off-message for a firm that is usually so clear about its position.