Helping consumers and businesses manage and plan their financial affairs, Financial Advisors (FAs) are the key intermediaries or channel for the promotion and distribution of a wide array of investment and insurance products and services. From life insurance, variable annuities, mutual funds and retirement products to trust services, wealth management and an endless assortment of investment instruments and securities, FAs are critical conduits connecting customers with financial services “manufacturers.”

Building enduring, strong relationships with Advisors is critical to providers that rely on this channel. Winning with Financial Advisors, however, is analogous to herding cats. The stakes and the challenges are greater than ever in this love/hate mutual dependency, making strengthening Financial Advisor experiences and relationships critical to winning with advisors.

The Financial Advisor Marketplace

The FA channel is a fire hose of “producers,” with an umbrella of titles from agents, broker/dealers, lawyers and accountants to money and wealth managers to financial planners, consultants and advisors. They might be solo practitioners, part of an independent agency or an independent RIA (Registered Investment Advisor) or embedded in a large wire house, bank brokerage or regional broker/dealer.

Insurance and investment companies are competing for the attention, business and allegiance of FAs in a dynamic market during particularly turbulent times.

- Boundaries separating banks from brokerage and investment companies have blurred, the line between insurance and investment firms is hazy and new FinTech competitors have burst on the scene.

- Aging Baby Boomers, the “mainstreaming” of retirement products and the explosion of the Mass Affluent Market have put a tidal wave of retirement/savings assets at stake.

- The market is fragmented: even the largest brands command only single-digit market shares.

- New market entrants, changing technologies, greater access to information and new products have spawned a variety of business models.

Customer Ownership

The Financial Advisor network is hyper-competitive and entrepreneurial. FAs strive to balance the interests of their clients with their own success, and they are fiercely protective of their customers, to whom they sell your products and services. Convincing them that your firm is the best partner with the best suite of support services for building the Advisor’s practice and meeting their customer’s needs is key to companies that rely on non-captive FAs.

As the point of contact for customer sales and service, the FA delivers the customer experience. This enables the FA to know their clients and their needs. But it also enables them to control the customer relationship.

For the company, this poses an obvious dilemma: FAs with strong customer relationships are good for business; but FAs can be fickle and leave, and their customers often follow.

Financial services providers may claim that the end consumer is their client. While the policy, security, contract or instrument may carry the name and legal obligations of the financial services company, make no mistake about it: the customer ownership and relationship scales tilt heavily in favor of the FA. A few salient points will clarify the customer ownership issue for those who are skeptical. Look at:

- The gaps in customer contact and other information in your customer files, bread and butter information for any firm managing customer relationships

- The lack of knowledge about customer prospects, inquiries and lost sales, critical performance information for firms that own their own distribution channels

- How orphaned accounts tend to languish once the FA exits the firm

- Who customers contact when they have an issue or question and the extent to which consumers often cannot even identify the underlying carrier or service provider, telling indicators of the entity with which customers identify.

This means that financial companies need to attend to the experiences and relationships of two sets of customers, both Advisors and the end consumer.

Defining the Advisor Relationship

Advisors are business partners with both shared and independent interests. This is a two-way relationship. The deeper, the “stickier,” the more mutually beneficial and compatible the business interests, the stronger the relationship.

At a practical level, the relationship is brought to life and defined in the form of “loyalty behaviors,” the actions that create (or destroy) value for a provider. These behaviors by Advisors include, for example:

- Continuing to offer and recommend a particular firm’s products and services

- Increasing the share of their business directed to a company

- Always including a firm in their “consideration set” for their customers

- Being open to new offerings (that is, extending “brand permission”) from a firm

- Recommending a company’s products and services to professional colleagues.

Maximizing loyalty behaviors maximizes the lifetime value (LTV) of FA relationships. Boosting the lifetime value of Advisors must be a central business objective of companies that use this distribution channel.

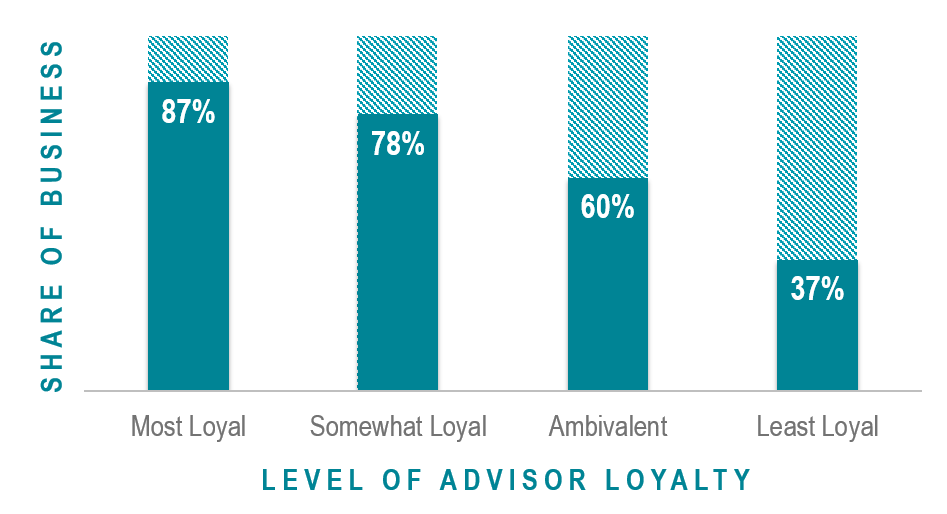

For example, Exhibit 1 illustrates the impact of an independent insurance agent’s loyalty to a life insurance company in terms of the share of their book of business written with that company. In one study we found that agents characterized as Most Loyal placed more than 80% of their business with that provider, while those who fall in the Least Loyal category delivered some one-third of their business to that firm. In other words, loyal agents “rewarded” the partners for whom they write insurance policies with almost 2.5 times the share of their book of business when compared to disloyal agents.

Exhibit 1: Case Study: Share of Business Independent Life Insurance Agents Place with a Provider by Level of Advisor Loyalty

The more loyal the FA, the more likely they are to stay a partner. This means a longer tenure for the Advisor/provider relationship, enhancing the lifetime value of FAs by lengthening their “lifetime.”

The Roots of Relationships

Loyalty behaviors don’t just happen randomly. FAs aren’t selling the products and services of one provider versus another based on whim. While they have a fiduciary responsibility to their customers, these behaviors are the result of business decisions made by Advisors based largely on their relationship and experiences dealing with a provider. The degree to which an Advisor is loyal to a provider is very much a function of the extent to which the provider plays a role in supporting the Advisor’s relationship with their customers.

Every financial services provider needs to identify and quantify the drivers of Advisor loyalty and measure their performance in the eyes of FAs. Based on our experience and previous research in this arena, we would expect attributes in Service, Support, Compensation and Business Development to be especially important, while features of Products, Returns/Costs, Communications, Image/Reputation and other issues tend to be less critical.

FAs inevitably will gravitate to the providers they think best facilitate the growth and support of their practice. This often translates into a keen interest in tools, materials and processes that support the sales and closing process. Anything that makes them look good and smart in front of clients is a huge plus. Inevitably time-stressed, they want firms that are easy to work with: this means quick (and positive) responses to their inquiries, flexibility in underwriting and other standards and minimizing administrative burdens. Advisors want to not just earn the maximum possible; they also want prompt, accurate payouts of commissions and fees and convenient tracking, as well as an easy (not to mention sympathetic) dispute resolution process.

FAs don’t present the products and services they promote as commodities; they want features and benefits that will appeal to customers and sell. Similarly, they want their customers to earn competitive returns so their customers stay happy and to minimize the barriers to selling. Corporate communications and marketing from the provider also are on the less-important side of the ledger for Advisors. They want to sell on behalf of firms with established names and unsoiled reputations, but this tends to be more of a table stakes “check-box” than a major driver of loyalty – as long as the firm doesn’t have a distinct PR problem that is a negative drag on business.

Building a VoA Program

Financial services providers that rely on an independent Financial Advisor channel need to complement their VoC (Voice of the Customer) research programs with a “VoA” (Voice of the Advisor) dimension. Conceptually similar to traditional VoC work, the VoA program must be driven by the firm’s business objectives with the Advisor community and be customized to the firm’s specific situation and needs.

The VoA program should be built to Best Practices standards for applied research to support and promote decisions to strengthen Advisor relationships. While measurement is essential, companies must turn the metrics into insights and action plans to drive change. Among other things, this requires linking results to business outcomes and financials to quantify the value of increasing Advisor loyalty to support investment decisions with a sense of ROI. This should be a programmatic effort, not simply a one-off project. Depending on a company’s need, the relationship research can include assessment of key experiences or can be supplemented by ongoing Advisor experience measurement following interactions at major touchpoints to make certain that the provider is delivering the Advisor with ongoing experiences that bolster overall loyalty.

Dependency on Financial Advisors is a reality for many financial services firms. The successful ones will be those that are the most effective at delivering experiences that cultivate and maximize the loyalty of their distribution partners.