According to Bloomberg, 8 out of 10 entrepreneurs fail within 18 months of starting their business. In fact, US Census Bureau’s Business Dynamic Statistics show that 400,000 businesses sprout up every year, while 470,000 shut their doors. As grisly as it sounds, this is the cold hard truth.

These bleak numbers, however, are not meant to dissuade new entrepreneurs. Instead, they should serve as a reminder that an overly optimistic approach to running your B2B venture may not be in your best interest. Anticipating the worst possible outcome and devising strategies to avoid or compensate for them can be the difference between you and the 80% of entrepreneurs who fail.

To stay prepared, it is imperative to understand why so many B2B startups crash and burn – and what you can do to prevent your startup from suffering the same fate. For that, you need to ensure that you don’t repeat the same mistakes and go down the rabbit hole.

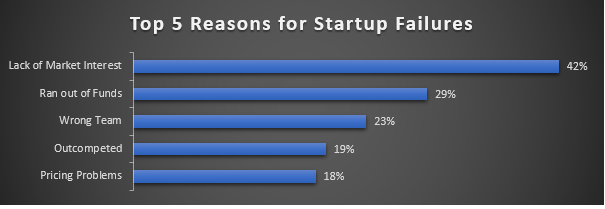

Let’s look at the most common reasons why most startups fail (see chart below):

Absence of the Right Market

Steve Jobs once quoted, “It’s really hard to design products by focus groups. A lot of times, people don’t know what they want until you show it to them.” While his words are immensely inspiring, they are also extremely dangerous. For every revolutionary product that creates a market for itself (like the iPhone or women’s razors), there are several others that fail to find their place.

The analysis of startup post-mortems shows that 42% of startups (out of which 44% B2B and 50% B2C) failed because there wasn’t a viable market for the product or service they were selling. Wealthfront’s co-founder and executive chairman, Andy Rechloff says, “If you are in a bad market with a good product, the market wins.” So, even if you have the most innovative product, it won’t matter if people aren’t willing to buy it.

How to Avoid This Fail:

Market research. Market research. Market research. If that didn’t make it clear enough, then let me spell it out for you: Before working on what you think will be the ‘next big thing’, you NEED to extensively study the market you’re about to enter. This is the most crucial step because your customers may not share your enthusiasm for your brilliant idea.

Some of the popular ways to do market research are:

· Do It on Your Own

One of the simplest ways to understand the market is by studying the companies that offer products or services similar to yours. You can determine the kind of marketing and advertising efforts will help you woo potential customers and get a better understanding of your audience.

You’ll most likely be competing with them for customers anyway, so keeping a close watch can prove beneficial even at later stages. You can also use research tools such as CensusScope, EdgarScan, and DataMonitor to get helpful data.

· Acquire Customer Data

Online surveys and focus group are valuable tools that help you understand how your target audience feels about your products or services. To find subjects, all you have to do is place an online ad and offer some form of compensation. Make sure that you set up a screening process to check if the applicants belong to the demographic you want to target.

· Purchase Reliable Data

There are many organizations or firms specializing in market research that routinely conduct detailed studies. Since collecting data can be a rather resource draining task, you may find it easier to buy the data you need instead. However, it’s possible that the research studies on the market you wish to target may not be available.

· Hire the Experts

Simply by acquiring data from various sources, you may not be able to get detailed insights. A research firm can manage the entire market research task and provide a thorough market analysis. If the cost of hiring a firm is stopping you from doing so, think about how many ad dollars you may end up wasting due to incorrect targeting and ineffective marketing communications.

Financial Difficulties

When you’re trying to run your startup like a racecar, you need to make sure that you don’t run out of fuel before you reach the finish line. Despite having a great product and market, many companies are forced to go belly up due to loss of funding.

For B2B startups, investor funding becomes even more crucial due to the long sales cycle and credit-based payment terms. Having problems with your cash flow can become fatal for your startup and that’s the last thing you need.

After MobileIgniter folded, one of their leaders wrote:

“What we found was that the sales cycle for the market we specifically wanted to go after is just way too long for a small company to absorb. Originally, we estimated that the sales cycle would be somewhere between three and six months. We then adjusted that to say it’s nine to 12 months … We hope to see IoT embraced by manufacturing and AG in the state and in the region. But it’s not going to be because of us.”

For a B2B business, having an ample cash reserve is a question of necessity, not choice. It helps in riding out periods of low sales and cashless business transactions.

How to Avoid This Fail:

Make it a practice to have a cash flow forecast ready to ascertain when you’ll need your next round of funding – either from an investor, personal savings, or in the form of a loan. However, if your business isn’t generating revenue and needs new funds frequently, then it’s bound to fail.

Many entrepreneurs are focused too much on developing the best product. They consider managing finances to be boring and assign this task entirely to their CFOs. As a startup CEO, you need to have an overall involvement in all aspects of your business.

As for the sales cycle, try to shorten it as much as possible. You might even want to reevaluate your business model. Let’s say that you’re developing a corporate communications and planner app. Instead of selling a year’s subscription upfront, you could offer a monthly and quarterly subscription as well. Another option would be to introduce a free 2-week trial or adopt a freemium model. This way, you give more users a chance to use your app and reduce their buying risk.

Not Having a Unique Value Proposition

Let’s look at the startup post-mortem of Hivebeat, a company that developed SaaS platform for organizations:

“We’ve tried all the things we wanted to try and we have a pretty good sense of what went wrong:

- We never hit real product/market fit. We built a product that was too generic for a very niche-based industry.

- Our product was great, but it wasn’t a 10x product. We had a much prettier product than the competition, but we were always lacking features in every niche.

- We were trying to do too many things at the same time. Both product-wise and marketing-wise.

- A transaction-based business model makes it hard to predict revenue, which made our growth curve look like a rollercoaster.”

According to the founders themselves, their product wasn’t differentiated or good enough to attract customers. This is true for many of the other failed startups (17% believe poor product to be the reason for failure). As mentioned earlier, 400,000 new businesses are born every year. It’s only natural that you weren’t the only one who had your ‘big idea’.

The only thing that separates you from the crowd is what you bring to the table. But, determining what that one thing is can be difficult for startups. In fact, you may spend the first couple of years to find the right product/market fit. For this reason, many startups make major changes to their initially planned targeted demographics, product attributes, or marketing style.

How to Avoid This Fail:

Unfortunately, there’s no quick and easy way to find your unique value proposition. All you can do is get your first few customers on board and pay attention to their needs. Once you have a more hands-on experience of dealing with customers belonging to a specific market segment, you’ll understand it better.

What your customers value in your business may force you to rethink your product and company values. Eventually, you’ll be able to realize what your offering should or shouldn’t entail. In some cases, the existing product is completely scrapped for a new product better suited for the audience. The startup may even shift its focus to a niche. It’s important that you are flexible with your outlook because if your startup doesn’t evolve, it will not last very long.

Conclusion

While these certainly aren’t all the only reasons why startups fail but they cover some of the major causes – and what you can do to prevent them. As the famous saying goes, “A wise man learns from the mistakes of others.” So, to avoid being just another number on the board, learn from other’s mistakes, and don’t repeat them while running your business.