Counterattack: Banks’ Field Guide to FinTech Disruption

As record levels of funding pour into FinTech ($131.5 billion globally in 2021), banks and credit unions are losing their status as primary financial services providers to U.S. consumers.

Banks are rightly concerned with the competitive threat posed by FinTech companies. However, far too many banks’ strategies for dealing with FinTechs are backward-looking (focused on protecting established products and business models) or dependent on broad, vaguely defined digital transformation initiatives.

Taking the FinTech Threat Seriously

According to research by Cornerstone Advisors, the percentage of Gen Z, Millennial, and Gen X consumers in the U.S. who consider a digital bank (like Chime, Cash App, or PayPal) to be their primary checking account provider has more than doubled since 2020. Furthermore, the percentage of Gen Zers whose primary checking account is with a megabank (like Bank of America, JPMorgan Chase, or Wells Fargo) has dropped from 35% in 2020 to 25% today. Among Millennials and Gen Xers, the percentages declined by nearly half during that span.

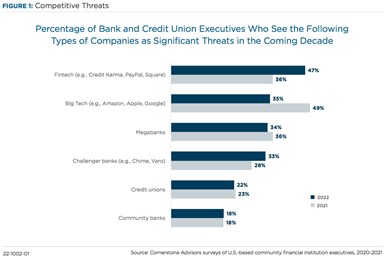

Therefore, it’s not surprising that 47% of U.S. bank and credit union executives said they see FinTechs as significant threats in the coming decade.

What Are Financial Institutions Doing About This Threat?

One response has been digital transformation – the re-architecting of technology, revamping of processes, and retraining of people to facilitate the delivery of digitally native financial products and experiences. In theory, that’s what banks and credit unions would need to compete with FinTech companies across the board. The trouble is that, in practice, there’s little evidence that banks and credit unions are close to actually achieving digital transformation.

The good news is that wholesale transformation isn’t required to effectively respond to FinTech competition. We should remind ourselves that FinTech itself isn’t some monolithic force consuming banking (though it’s sometimes discussed that way). FinTech is thousands of companies, each individually trying to disrupt banks across hundreds of different products and customer segments.

Fighting back against FinTech isn’t an exercise in total war, but rather in carefully picking one’s battles.

Let’s focus on five specific competitive threats – overdraft; saving and investing; buy now, pay later (BNPL); niche neobanks; and open banking. We’ll discuss what U.S. FinTech companies are doing in these areas to gain traction in the market and what banks should be doing to counter them.

1. Overdraft

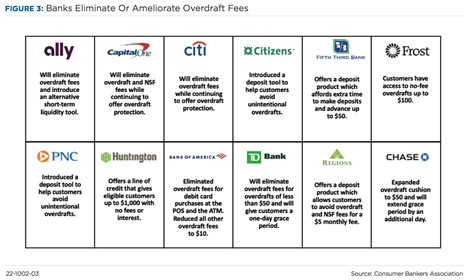

Neobanks have made fee-free overdraft protection a central and highly visible product feature. Given that U.S. banks collected $15.47 billion in overdraft and non-sufficient funds (NSF) fees in 2019, this fee-free feature has provided neobanks with substantial competitive differentiation in the market.

Generating significant revenue from overdraft and NSF fees is now competitively and regulatorily unsustainable for banks. Forward-thinking banks are recognizing the unsustainability of their current offerings and making proactive adjustments.

How Banks Should Respond

Significantly reducing the rate of accidental overdrafts (or not penalizing such overdrafts) is a good start, but banks shouldn’t lose sight of the value that intentionally used overdraft protection (or similar short-term lending products) can have for customers facing cash flow imbalances.

Solving for this short-term liquidity need without benefitting from excessive overdraft fee income will be challenging, however, this shift presents opportunities for banks that are ready for it. As the Chief Strategy Officer at a top-20 U.S. bank explained, “For institutions that are really good at underwriting short-term consumer credit, this moves the battleground from an undifferentiated commodity to a space where you can meaningfully differentiate based on the relationship you have with the customer and the data that you can incorporate into your underwriting.”

2. Saving and Investing

There are two jobs to be done in this area – helping consumers set more money aside for saving, and helping consumers earn the best possible yield on that money (within their risk tolerances). For both of these jobs, consumers are increasingly turning to FinTech apps.

The threat posed by FinTech savings and investment apps (especially apps that combine these functions) isn’t the introduction of new competitors for banks’ savings and investment products – it’s the potential for these apps to wrest control over the allocation decisions that fund those products. By automating the actual money movement process and providing consumers with a variety of high-yield investment options, FinTech apps can significantly reduce the need for consumers to log in to their primary banks’ mobile apps.

Given the fact that only 12% of consumers are using an automated savings tool from their bank or credit union (based on a Q1 2022 Cornerstone survey), there’s clearly room for growth.

How Banks Should Respond

Banks need to sharpen their strategic responses to this competitive threat on two fronts:

1. Refining the experience and insights provided by their savings tools

While automated savings tools are relatively common offerings from banks today, there is more work to be done to ensure that they are as useful as possible to consumers – particularly low-income consumers.

2. Blending savings and investing together

Automating the process of setting money aside is useful to customers, but in a low-rate environment, banks should also be offering a variety of different yield-generating investment opportunities (across a wide spectrum of risks). Otherwise, they aren’t providing a truly competitive alternative to FinTech.

Banks will also need to be less squeamish (although still responsible) about new investment asset classes, such as cryptocurrencies – a step that many banks are still unwilling to take.

3. Buy Now, Pay Later

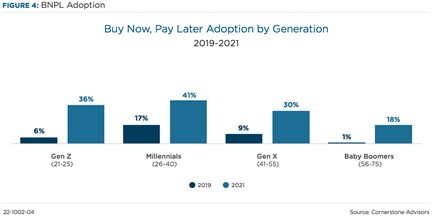

Buy now, pay later (BNPL) has exploded in popularity over the last few years.

According to Cornerstone Advisors consumer surveys, the percentage of Gen Zers making purchases with BNPL plans grew six-fold between 2019 and 2021.

BNPL’s superpower is the ability to significantly improve conversion rates and average order value without taking on excessive, long-term credit risk. It does this by constraining the loan parameters – most BNPL loans are paid in four installments within six weeks, often for less than $200 – which minimizes the risk of each individual loan, while collecting fees from merchants (allowing the BNPL provider to offer the service to consumers for free or very inexpensively).

BNPL has become extremely popular with merchants and accessible to consumers across every credit score band. This makes it a dangerous competitor to banks’ payment and unsecured lending products. A recent estimate from McKinsey shows that FinTech companies providing BNPL products have already siphoned $8 billion to $10 billion in annual revenues from banks.

Many bank executives are strangely blasé about the competitive threat posed by BNPL. In spite of its growth and obvious appeal, especially with young and digitally native consumers, the general sentiment is that the consumers who use BNPL aren’t the ones these banks would want as customers anyway (due to credit risk concerns).

How Banks Should Respond

The truth is that consumers are going to use BNPL, regardless of what banks think about it.

Retroactively attaching BNPL capabilities to credit cards is an appealing approach for banks – it preserves existing interest and interchange revenue streams, and doesn’t require building direct partnerships with individual merchants. However, it’s a shortsighted approach because:

- Today’s credit-invisible consumers are tomorrow’s prime credit customers. A lot of Gen Zers fall into the subprime and credit-invisible consumer segments, and for many of them, BNPL is their first credit product (i.e. their on-ramp into the credit system). Once they become prime banking customers, the BNPL providers that helped them get there will have the inside track on earning and keeping their business – in lending and beyond.

- Banks’ customers need help managing their BNPL activity. Over the past two years, 43% of BNPL users have made one or more late payments. Two-thirds paid late because they lost track of the bill’s due date.

Emerging evidence suggests that some consumers will struggle to use BNPL responsibly (especially across multiple providers). There is an opportunity for banks to help these consumers more effectively manage these loans. If banks care about acquiring younger customers or helping consumers manage their financial health, they cannot sit BNPL out.

4. Niche Neobanks

A side effect of the massive investment in FinTech is the emergence of a robust set of FinTech infrastructure companies – everything from banking as a service (BaaS) platforms to modern card issuing, processing, and servicing systems. As a result, the upfront time and cost to launch a new consumer or small business neobank have dropped significantly. This has led to the creation of an entirely new category of financial services providers: niche neobanks.

The niche banking concept works by finding a specific segment of consumers that share a common set of functional and emotional needs when it comes to money. The neobank builds differentiated financial products and leverages those consumers’ existing groups and communities to distribute products.

Niche neobanks’ intense focus on specific customer segments gives them an advantage over most traditional banks in understanding the pain points of their target customers (at a very granular level) and building products and experiences that address those pain points. Differentiated products enable niche neobanks to “pick out” small portions of banks’ customer bases, which is a threat that can seem trivial on an individual level but becomes far more serious in the aggregate.

How Banks Should Respond

Competing with niche neobanks will require banks to dramatically reduce the time and expense it takes to launch new products. With that agile product development ability unlocked, banks should then seek out specific customer segments with financial needs that are either unmet or inadequately addressed and build products for them. These segments can be professions or even hyper-specific life stages.

5. Open Banking

Open banking – which we’ll define as the ability for consumers to share data from their financial accounts and providers in order to enable other products or experiences – is a core function of many FinTech apps on the market today. As adoption of FinTech has increased, the number of consumers using open banking capabilities to fund a new deposit account or power ongoing financial management insights has also increased.

A natural consequence of this growing use of open banking is that more consumers have come to view such capabilities as critically important. According to research commissioned by Plaid, 80% of U.S. consumers agreed that, “It is important to be able to connect my bank account to the digital finance apps and services I choose.” 69% of Americans said, “I would consider switching banks if my primary bank could not connect to my financial accounts.”

Banks don’t like open banking. The idea of sharing proprietary customer data with competitors in order to make those competitors’ products easier to use is obviously unappealing to incumbents. However, this is no longer a defensible position to try to hold. Regulators like the CFPB, which is in the midst of rulemaking on open banking through Section 1033 of the Dodd-Frank Act, also view open banking as a critical tool for leveling the competitive landscape.

Bottom line: banks that make it difficult for customers to share data are putting those relationships at risk and painting a regulatory bullseye on their backs.

How Banks Should Respond

Open banking is going to happen, whether banks want it to or not. They might as well benefit from it.

Many banks have begun to work with data aggregators to replace screen scraping with more secure and performant APIs. Building common standards and streamlining technical integrations is a necessary first step. However, the second step, which is one that few if any banks have taken, is to leverage these APIs (and consumers’ willingness to permit access to their data) to build new products and services.

Apart from specific instances – like FICO’s UltraFICO Score, which enables banks to augment traditional FICO scores by allowing consumers to share their deposit account data – banks have been strangely reluctant to use open banking to their advantage. Meanwhile, FinTech services (such as BNPL) are making it more complex for consumers to manage their finances.

Utilizing open banking, banks could build new financial management capabilities that pull data together from these disparate FinTech providers and deliver unified insights to their customers that could help them protect and improve their financial health.

Conclusion: Preparing for the Battles Ahead

Looking across the five FinTech threats that have been outlined, there are a number of common challenges that banks will need to overcome if they want to effectively respond to FinTech disruptors. Specifically, the following steps are recommended:

1. Build more comprehensive customer data profiles. Consumers have never had more choices than they do today. Banks must ensure that they have a comprehensive view of their customers’ financial behavior across all the providers they choose to work with.

2. Invest in more sophisticated risk decisioning. Competition from FinTech has significantly cut into banks’ profit margins, particularly with higher-risk customers. Banks are increasingly facing a choice – cede ownership of younger and higher-risk customers to FinTech or sharpen risk decisioning capabilities (leveraging more comprehensive customer data) to compete effectively.

3. Prioritize software development agility. Making even simple modifications can sometimes take banks years to execute, which means more complex changes are practically impossible. Banks must invest in structural changes to accelerate software development and deployment cycles.

4. Build for developers. As an executive responsible for strategic partnerships at a top-10 U.S. bank told Cornerstone Advisors: “Banks’ customers are now developers. You have to modularize your capabilities so that developers, inside your bank and outside of it, can assemble new products and experiences quickly and inexpensively.”

5. Adopt a competitive mindset. Banks spend far too much time and energy fighting change rather than embracing the competitive possibilities that change brings. The disruptions introduced by FinTech should be viewed as opportunities to innovate and improve your bank’s competitive position in the market. If you don’t, the market will pass you by.

Read the full report by FICO and Cornerstone Advisors here – Counterattack: Banks’ Field Guide to FinTech Disruption