Ever since Air Canada started the process of divesting its Aeroplan Frequent Flyer Program (FFP) in 2005 — the global loyalty zeitgeist has seen virtually every loyalty consultant, major consulting firm, coalition program operator, financial analyst, and long-term “loyalty insider” — place Air Canada and Aeroplan on a pedestal whilst preaching the new-world-order of FFP spinoffs.

If you were to listen to the propaganda of the pro-spinoff brigade over the last decade, you would likely believe that spinning-off your FFP could even solve world peace.

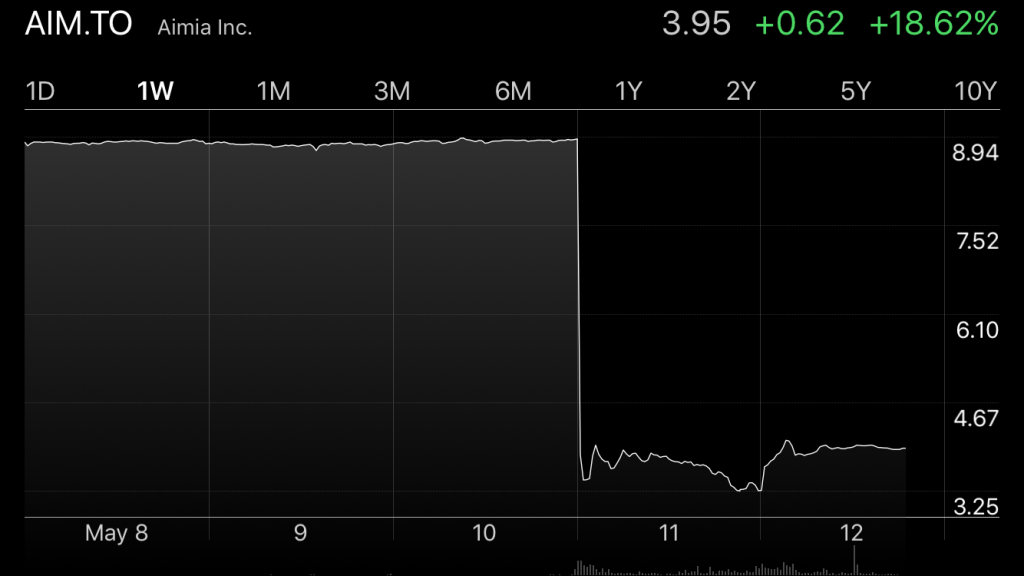

That all came crashing down yesterday, with the tectonic-plate-shifting news that Air Canada and Aeroplan will be divorcing in 2020. Air Canada has decided to (re)launch its own FFP and bring the program in-house.

Aeroplan will continue to be able to purchase seats from Air Canada at market rates, but will no longer have access to 8% guaranteed inventory, and will no longer have access to sought-after Star Alliance redemption seats.

The response has been seismic in nature.

First — Aimia Inc. (the parent company of Aeroplan) had its stock re-accommodated to the tune of around 57% at the time of writing.

Most of the lost market capitalization has been transferred to Air Canada’s stock.

And now — the industry responds.

“The spin-off of loyalty programs is dead. Well, it was never really alive” — Global Flight

CEO of Global Flight, Ravindra Bhagwanani — offered this honest and direct critique of the spin-off brigade

“While no other airline bought into the logic of Aimia to fully spin off its FFP, Aimia nevertheless managed to get more than one person in the industry confused and to talk about the “advantages” of spin-off models — forgetting that this business model never made sense for a cash-healthy airline, but unilaterally for the program operator/investor only. There is no doubt about the value they’ve managed to bring to the Aeroplan program, but that is only one side of the truth. Focusing unilaterally on that aspect was, at best, alternative facts building. At the end of the fact, Aeroplan always remained the FFP of Air Canada from a customer perspective.”

“Loyalty Insiders” tend to sound a lot like an echo-chamber, often parroting the same press-release sound-bytes. But Ravindra bravely breaks from the pack and calls it how he sees it…

“First, full spin-off of loyalty programs don’t work as they create a strategic and financial gap between the “moral” and financial owner of the program. If the players in the only true spin-off constellation we had in the market and which was praised as the example par excellence for everybody to follow comes to that conclusion, there is nothing more to add here.”

And, just in case you were in any doubt…

“And now watch out for all the self-proclaimed specialists out there making their comments — after having followed the logic of Aimia over more than a decade (and often even having been part of it!). There were very few consistently critical voices about the spin-off model in the market, but everyone is now obviously trying to position himself for the future, unfortunately too often by creating another sort of alternative facts. About themselves.”

Another viewpoint came from a senior executive who runs the FFP of a global international airline, who took the time in an early morning phone call to ask me…

“Can we please get a list of everyone who has said spinning-off loyalty programs is a good idea, and publish their names as #fakeloyaltyprofessionals, because now everyone will jump on the pro Air-Canada bandwagon, even though they may have been pro spin-off previously.”

With those direct views — it looks like there may be plenty of safe space on the fence…

So… Are Loyalty Program Spinoffs Dead?

Let’s not panic about the 57% drop in Aimia’s share price.

A more sober discussion of the merits of program spinoffs is needed.

First — let’s call it now — we’re not likely to see any 100% divested FFPs anytime soon — in fact, the Air Canada split probably makes any public spinoff less likely.

I spoke with Airline Weekly’s Managing Partner Seth Kaplan, who told me “I think what happened this week will make divestitures less likely, because investors in any potential loyalty program spin-off IPO would apply a discount to the spun-off company, realizing the risk of investing in a company that is so reliant on one other company.”

One of the key challenges of a separate FFP, is the challenge of a bifurcated strategy.

An airline loyalty program has two separate, yet interlinked goals:

1/ Generate increased loyalty to the host airline, including driving an uplift in core airfare sales, incremental revenue, increased share-of-wallet, and creating switching costs for customers (who are afraid to lose status benefits);

and

2/ Being cash-generative in its own right, by selling points to program partners— which we have discussed at length in previous articles. See “Is American’s Loyalty Program Worth More Than The Airline?”.

When an airline maintains its program “in-house” — it has ownership not just of the program, but of the entire customer relationship.

There’s only one CRM system, and only one point of contact for the customer. Only one website for the customer to visit, and no confusion around the difference between the “points program” and the “elite status program” as there was with Air Canada.

There’s also a singular “alignment of interests” with an in-house program.

A spun-off program can bring supposed benefits (which we’ll explore below), but can easily create a “conflict of focus” with loyalty program executives focusing solely on growing points-sale revenue, expanding partner earning opportunities, and filling their teams with email marketing interns; at the expense of growing “loyalty” with the airline’s best customers.

THE CASE FOR SPINOFF…

Let’s be clear — most spinoffs have occurred during a period of financial distress for the host airlines.

In Seth Kaplan’s words, “Generally speaking, successful airlines don’t spin off their loyalty plans. It’s almost always done out of desperation”.

This is also the major lure for financial analysts who see the opportunity to “unlock hidden value”. (Let’s be sure to add that to the Buzzword Bingo list).

A recent report by Stifel analyst Joe DeNardi into the profitability of U.S airline Frequent Flyer Programs put the topic of program spinoffs back on the discussion table.

DISCLOSURE: I contributed research and analysis to the Stifel report. I do not hold stocks in the airlines mentioned, nor do I provide investment advice.

Whilst not the only factor, a quick cash injection is clearly a primary motive.

Management Focus

An additional issue for loyalty programs (and a source of tension for program managers), is that loyalty programs are complex businesses.

Most people that work at loyalty programs aren’t loyalty people. Most are basic marketing folk. Think email marketing, creative, data analytics, campaign management and reporting etc.

Most programs only have a couple of key individuals who truly understand loyalty. It’s a very specialized skill-set.

As you can also imagine — most senior airline executives have been in the industry for a long time. Either a lifetime at the one airline, or perhaps an entire career between different airlines. That also requires a particular skill-set.

Traditional airline executives know how to bank hubs, hedge fuel, densify aircraft, and manage routes. Clearly — these are very different skills than those required to manage loyalty programs.

This usually means that airline executives fail to fully understand and appreciate the nature of the loyalty program (although they are aware of its cash-generative nature), and often make strategic decisions that undermine the program.

Additionally — due to competing requirements, traditional airline executives tend to bias cash investment into airline operations which they are more familiar with, even though the loyalty program may actually generate better returns.

Some loyalty managers argue that spinning off is the only way to convince dinosaur airline executives to actually invest in FFPs.

This is why investors commonly make the argument that the airline and loyalty program are worth more separate than together. Investors see the opportunity for separated entities to each invest and make decisions that better themselves.

I asked Seth Kaplan about how an external program could be more focused…

“An external loyalty program has the benefit of not having to “serve two masters,” so to speak — that is, optimize for both driving loyalty and for the program’s own profitability. An external program clearly optimizes for the program’s profits.”

“Of course, with an in-house program, an airline might conclude that something that isn’t most profitable for the program is still more profitable for the airline as a whole (for example, if the program nonetheless shifts travel share to the airline).”

Clearly this tension between the recognition/status program, and the points program can lead to sub-optimal outcomes.

Air Canada has made no secret of the fact that it wants more control of the holistic customer relationship, as well as feeling ‘locked-in’ with its award seat obligations to Aeroplan.

Complications

Other issues with separated programs can arise with data ownership, not just of the customer relationship, but in regards to data privacy, data-sharing with program partners, consumer insights, and cross-partner promotions.

There can also be conflict and tension between partners of the external loyalty program, and partners where the airline owns the relationship — such as alliance or joint-venture airlines.

Brand and licensing issues can complicate matters, and even add a point of friction to the customer experience.

Virgin Australia is one of the more recent entrants to the spinoff club, divesting 35% of its Velocity Frequent Flyer program in 2014.

But members are constantly complaining about the clunky nature of having to login to two separate websites, and that the airline has lost focus on looking after its best customers, whilst the loyalty program has been preoccupied with selling points to more partners.

Additionally, Velocity launched its Global Wallet membership cards, which feature a prepaid Visa card on the back of the frequent flyer card.

The problem — licensing issues prevented them from displaying the Virgin Australia logo on the card.

Members frequently reported showing up at partner airline lounges overseas, to find lounge agents denying entry as “We don’t partner with ‘Velocity’, only ‘Virgin Australia’”.

Separate Reporting

There is a compromise position that works well.

Some airlines make an effort to report the performance of their FFPs separately.

Some simply report as a separate business unit, others like Qantas actually separate their FFPs into their own fully-owned subsidiary.

This provides many of the benefits of a separate program, without compromising the strategic alignment of both the airline and FFP.

Greater transparency allows greater focus on both the core airline operation (without the FFP’s positive results masking the airline’s poor results), and also forces airline executive to be more aware, and pay more attention to, the FFP and the decisions which impact its profitability.

Whilst DeNardi emphasizes that he is not suggesting loyalty programs be spun-off, his report makes clear that airline mileage revenue is underappreciated by the market, and that there is significant upside potential to airlines to increase disclosures.

This is a position that we strongly support.

Rather than spinning-off their programs, DeNardi suggests that airlines report their loyalty programs as a separate entity. He uses the United Loyalty Services model from 2002–2005 as an example airlines should follow.

We would suggest that the best model for airlines to follow is that of Qantas, which reports its Qantas Frequent Flyer program as a separate entity. This has also allowed it to realize additional revenue through commercialization of its Qantas Loyalty brand.

However it wasn’t all roses for the Qantas program, even as a separate entity.

Airline industry insiders familiar with the program often described the Qantas program as “lazy, bloated and inefficient”, especially prior to Virgin Australia relaunching its own FFP with an aggressive status match campaign in 2011.

And Qantas’ perceived market dominance let it to become what insiders described as “cocky”, resulting in several high-profile commercial partners being unhappy with the program and leaving — including Australian grocer Woolworths and telecommunication provider Optus.

But many argue that these issues weren’t a result of being a separate entity, and would have just as likely occurred with an in-house program.

SUMMARY

I’m a spin-off skeptic, but that’s due to issues of strategic misalignment and bifurcation of focus.

There are clearly benefits that “can” be realized by a partial spin-off – IF VERY CAREFULLY – managed and designed.

I’m not convinced that any of the programs thus far have demonstrated a model implementation.

On the other hand — like a good magistrate — I’m always open to be persuaded by solid arguments.

Investors on the other hand are more easily spooked — and it’s pretty safe to say that spinoffs, if not dead, are on life-support for now.

It’s time for some serious reflection about the wisdom and prudence of spinning off your Frequent Flyer Program.

This conversation is long overdue, and only just beginning…