The CDP industry had a great 2018, growing by 60% and reaching $740 million revenue, according to the CDP Institute’s just-released Industry Update (click here to download). The industry added 29 vendors and 2,653 employees, slightly more than the 26 vendors and 2,233 employees added in 2017. Vendor funding increased $568 million in 2018 vs $492 million in 2017.

But the smooth growth hides some interesting twists. The report period (second half of 2018) saw the first two major acquisitions of CDP vendors: Datorama by Salesforce for reported $800 million and Treasure Data for $600 million by ARM Holdings for reported $600 million. It saw a new generation of purpose-built CDP systems for vertical industries and personalized messaging. There was a sharp drop in new CDP funding. And increased competition from non-CDP vendors is clearly on the horizon.

One thing that didn’t happen was the long-expected industry consolidation. New vendors are being added more quickly than existing vendors can grow – so the industry is becoming more fragmented.

Let’s look at each of these developments in more depth.

Acquisitions. The CDP industry had already seen quite a few small acquisitions, mostly by agencies or vertical industry specialists adding customer data management to their existing product lines. But Datorama and Treasure Data were the first acquisitions of large CDP companies. They were surely the first over $100 million and possibly the first over $10 million.

Yet neither deal is a simple as a large marketing suite adding a CDP module. Salesforce is a marketing suite vendor but it purchased (and so far is selling) Datorama as a marketing performance analysis tool. This is how Datorama had positioned itself before the acquisition, even though Datorama does have a few clients using it to manage individual-level customer data in true CDP fashion. ARM Holdings, itself owned by tech conglomerate SoftBank, is a chip technology company that purchased Treasure Data to manage Internet of Things data. (Treasure Data will continue selling itself as a conventional CDP.) Yet, regardless of their intent, Salesforce and ARM are likely to find their clients using their acquisitions for CDP-style customer data management. Demand for such solutions is simply too strong to avoid that happening. And you can be sure that clever salespeople at both companies will offer the products as CDPs if that’s what it takes to close a deal.

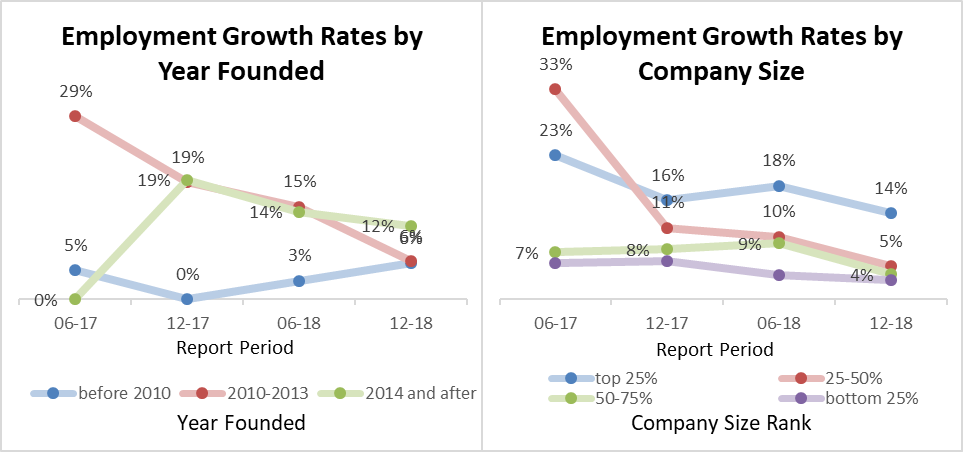

Next-Generation CDPs. Nine of the vendors added during the period were founded in 2014 or later – the first time a majority of new entrants were this young. These companies are small and lightly funded, averaging just 25 employees and $4 million. They can be seen as “CDP natives” that were designed from the start as CDP systems. By contrast, the majority of vendors entering the industry in earlier periods were older, larger, and better funded. Most began as something else and later repositioned as CDPs.

The new firms included more data access and analytics vendors than previous periods, again indicating that they were purpose-built for specific CDP applications and industries. This is the first period since reporting began that the industry share of campaign vendors decreased.

Organic Growth and Fragmentation. Most industry growth in the past two years– a remarkably constant 72%, as it happens — has come from new vendors, not organic growth by existing vendors. One implication is that adding younger, smaller companies could reduce the industry growth rate. Whether this happens depends on how quickly the existing vendors grow. So far, employment at existing firms has increased around 10% per six-month period, which translates to a healthy but unspectacular 20% per year. One cause for optimism: younger firms have tended to grow faster than older firms, suggesting the rate might increase as more young firms appear.

Larger firms have also grown faster than smaller firms. Ordinarily this would result in higher industry concentration, but so far the entrance of new firms has more than outweighed this effect. The industry share of the five largest vendors has in fact decreased from 46% in the first report to 28% in the latest report. I expect this fragmentation to increase as more specialized CDP vendors carve out niches in particular industries, regions, and functions.

Funding. We measure funding in two ways. One looks at aggregate funding for all industry vendors; this grows as new vendors are added, regardless of when the funding took place. The other approach looks at the timing of funding events. It includes events that happened before a vendor joined the industry. The first measure, aggregate funding, has increased in rough parallel with industry vendors and employment. The second measure is more volatile and shows a sharp decrease since its peak in the second half of 2017.

The patterns of the funding have also changed over time. In 2018, little funding went to data access firms, companies founded before 2010, or the five largest companies (accounting for 25% of industry employment) even though those are still a major portion of the industry. This suggests that those firms had already acquired ample funding to support their growth.

The decline in new funding during the most recent period may mean that investors are becoming cautious about supporting new CDP vendors. Whether this slows industry growth remains to be seen: the smaller, niche CDP vendors are more able to finance their early activities from personal investment and operations. It’s likely that the more successful of these will attract additional funding in the future.

External Competition. There’s nothing in the CDP industry data to capture external competitors. But last fall saw announcements of products addressing the same needs as CDPs by Salesforce, Oracle, and an Adobe/Microsoft/SAP alliance. My take is that the Oracle and Adobe entries are architecturally similar to CDPs as we define them (“packaged software that builds a unified persistent customer database accessible by other systems”) while the Salesforce entry falls short because it doesn’t create a persistent database. None of these products is fully operational but the announcements alone will deter some buyers from purchasing alternatives. We’ve also seen many personalization and delivery system vendors beef up their customer data management capabilities in ways that make them more CDP-like. There’s no doubt that the growth of the CDP industry has captured other vendors’ attention, both as an opportunity for expansion and as a threat to their existing business. Competition from these vendors can only increase as they better understand the capabilities needed for a CDP.

We’ve also seen existing CDP vendors expand their own footprints, often by adding email delivery capabilities. These are offered as a convenience for their clients, not because the CDPs want to enter the email business. But the result is to further blur the distinction between CDPs and other systems.

The net impact of these changes on independent CDP vendors is still in doubt. Some companies will surely prefer to buy a CDP that’s a component of their existing delivery system or marketing suite. But all will become more educated about true CDP requirements and many will find that these are best met by a separate product. Pressure from buyers may also force delivery systems and suite vendors to open up their products to external connections, both to feed data to an external CDP and to read CDP data. This greater openness will make it easier to use an independent CDP and thus reduce the benefits of buying a CDP that’s built into a larger system. If analysts who predict a world of microservices plugged into central platforms via standard APIs are correct – I’m looking at you, Scott Brinker – then independent CDPs will prosper within this open future environment.